Press Releases

NEW YORK, Feb. 21, 2017 /PRNewswire/ -- Data through January 2017, released today by S&P Dow Jones Indices and Experian for the S&P/Experian Consumer Credit Default Indices, a comprehensive measure of changes in consumer credit defaults, shows the composite rate up three basis points from the previous month at 0.92% in January. The bank card default rate recorded a 3.21% default rate, up 26 basis points from December. Auto loan defaults came in at 1.06%, up three basis points from the previous month. The first mortgage default rate was 0.72%, up one basis point from December.

All five major cities saw their default rates increase in the month of January. Miami had the largest increase, reporting 1.67%, up 14 basis points from December. Miami's composite default rate is at a 31-month high. Dallas and Los Angeles both reported eight basis point increases from the previous month at 0.75% and 0.80%, respectively, in January. Chicago saw its default rate increase five basis points to 1.03%. New York reported a default rate increase of one basis point from the last month at 0.88%.

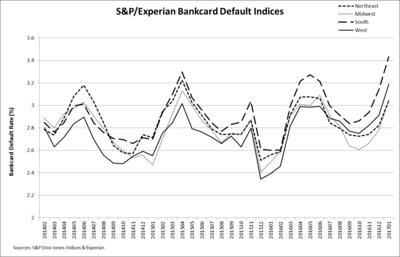

When comparing the bank card default rates among the four census divisions, the default rate in the south is considerably higher than the other three census divisions.

"While consumer credit default rates on mortgages and auto loans remain low and stable, default rates on bank cards have popped up to the highest level seen since July 2013," says David M. Blitzer, Managing Director and Chairman of the Index Committee at S&P Dow Jones Indices. "Recent data point to consumer optimism: retail sales rose 5.5% in January 2017 compared to a year earlier, consumer sentiment measures rose over the last two years, and employment and labor market conditions are favorable. Federal Reserve data on consumer credit and mortgage debt outstanding reveal that consumers are borrowing money.

"Current default levels do not present any immediate concerns for the economy. During 2004-2006, a period of strong retail sales and consumer spending, bank card defaults were higher than today. Moreover, even if interest rates were to increase much faster than the Fed or most analysts currently expect, the cost of borrowing money is unlikely to create problems for consumers. The weak spot, if there is one, would come with a rise in unemployment and an economic downturn."

The table below summarizes the January 2017 results for the S&P/Experian Credit Default Indices. These data are not seasonally adjusted and are not subject to revision.

|

S&P/Experian Consumer Credit Default Indices |

||||

|

National Indices |

||||

|

Index |

January 2017 |

December 2016 |

January 2016 |

|

|

Composite |

0.92 |

0.89 |

0.96 |

|

|

First Mortgage |

0.72 |

0.71 |

0.84 |

|

|

Second Mortgage |

0.48 |

0.41 |

0.65 |

|

|

Bank Card |

3.21 |

2.95 |

2.52 |

|

|

Auto Loans |

1.06 |

1.03 |

1.04 |

|

|

Source: S&P/Experian Consumer Credit Default Indices |

||||

|

Data through January 2017 |

||||

The table below provides the S&P/Experian Consumer Default Composite Indices for the five MSAs:

|

Metropolitan |

January 2017 |

December 2016 |

January 2016 |

|

|

New York |

0.88 |

0.87 |

1.04 |

|

|

Chicago |

1.03 |

0.98 |

1.02 |

|

|

Dallas |

0.75 |

0.67 |

1.11 |

|

|

Los Angeles |

0.80 |

0.72 |

0.72 |

|

|

Miami |

1.67 |

1.53 |

1.17 |

|

|

Source: S&P/Experian Consumer Credit Default Indices |

||||

|

Data through January 2017 |

||||

For more information about S&P Dow Jones Indices, please visit www.spdji.com.

ABOUT S&P DOW JONES INDICES

S&P Dow Jones Indices is the largest global resource for essential index-based concepts, data and research, and home to iconic financial market indicators, such as the S&P 500® and the Dow Jones Industrial Average®. More assets are invested in products based on our indices than based on any other provider in the world. With over 1,000,000 indices and more than 120 years of experience constructing innovative and transparent solutions, S&P Dow Jones Indices defines the way investors measure and trade the markets.

S&P Dow Jones Indices is a division of S&P Global (NYSE: SPGI), which provides essential intelligence for individuals, companies, and governments to make decisions with confidence. For more information, visit www.spdji.com.

About Experian

We are the leading global information services company, providing data and analytical tools to our clients around the world. We help businesses to manage credit risk, prevent fraud, target marketing offers and automate decision making. We also help people to check their credit report and credit score and protect against identity theft. In 2015, we were named one of the "World's Most Innovative Companies" by Forbes magazine.

We employ approximately 17,000 people in 37 countries and our corporate headquarters are in Dublin, Ireland, with operational headquarters in Nottingham, UK; California, US; and São Paulo, Brazil.

Experian plc is listed on the London Stock Exchange (EXPN) and is a constituent of the FTSE 100 index. Total revenue for the year ended March 31, 2016, was US$4.6 billion.

To find out more about our company, please visit http://www.experianplc.com or watch our documentary, "Inside Experian."

Experian and the Experian marks used herein are trademarks or registered trademarks of Experian Information Solutions, Inc. Other product and company names mentioned herein are the property of their respective owners.

FOR MORE INFORMATION:

David Blitzer

Managing Director and Chairman of Index Committee

New York, USA

(+1) 212 438 3907

david.blitzer@spglobal.com

Soogyung Jordan

Global Head of Communications

New York, USA

(+1) 212 438 2297

soogyung.jordan@spglobal.com

Matt Tatham

Experian Public Relations

917 446 7227

matt.tatham@experian.com

Jointly developed by S&P Dow Jones Indices LLC and Experian, the S&P/Experian Consumer Credit Default Indices are published on the third Tuesday of each month at 9:00 am ET. They are constructed to track the default experience of consumer balances in four key loan categories: auto, bankcard, first mortgage lien and second mortgage lien. The Indices are calculated based on data extracted from Experian's consumer credit database. This database is populated with individual consumer loan and payment data submitted by lenders to Experian every month. Experian's base of data contributors includes leading banks and mortgage companies, and covers approximately $11 trillion in outstanding loans sourced from 11,500 lenders.

For more information, please visit: www.consumercreditindices.standardandpoors.com .

SOURCE S&P Dow Jones Indices