Press Releases

NEW YORK, Dec. 19, 2018 /PRNewswire/ -- Pricing across the global energy markets will face headwinds in 2019, with a weaker and more uncertain macroeconomic framework deflating price formation in general, according to two special reports just issued by S&P Global Platts Analytics. Such headwinds will require the industry and portfolio managers to take a big-picture approach.

"One of the key lessons learned in 2018, painfully by some, is that market sentiment can shift violently without much change in fundamentals, requiring a steady, holistic perspective," said Chris Midgley, global head of analytics, S&P Global Platts. "It is clear that this volatility will remain a feature across the energy markets in 2019, particularly as IMO 2020 nears."

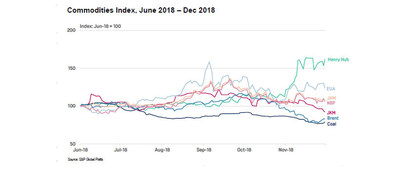

Particularly blustery head winds are in store for markets where prices finished 2018 at elevated levels, and well above costs, such as North American natural gas and global coal. However, if the supply side can adjust to the reality of slowing demand growth, energy prices can find support. For natural gas liquids (NGLs), the ongoing logistical constraints at the US Gulf Coast are likely to manifest on continued price volatility, particularly for ethane and liquid petroleum gas (LPG), over the next year despite strong global demand.

LPG, such as propane and butane and used in transportation fuel, refrigeration, heating and cooking, is rapidly facing US export capacity constraints, especially along the US Gulf Coast. For LPG feedstock propylene, there is clear potential for high volatility globally over the next 12-18 months.

Analysts at S&P Global Platts see weakening prices of Henry Hub natural gas. The slowdown in US demand growth will exceed that of supply. But if winter temperatures prove to be colder than normal, near-term prices will need to move higher to bring on enough supply to replenish depleted storage levels.

For global liquefied natural gas (LNG), it will be end-user-backed LNG demand that faces particular struggle to cope with the speed and force of new supply entering the market in 2019. Non price-responsive demand in Asia will be easily met and JKM spot physical prices (reflecting LNG as delivered into Japan, Korea and China) will sag next year.

Access the full S&P Global Platts Analytics Top Factors to Look Out For in 2019 for Energy here. Among the 22 key take-away themes:

- NGL supply growth will strain the North American energy system

- Saudi Arabia will need to be nimble to balance 2019 oil supply

- US oil supply limited by pipelines

- Oil demand slowing: trade war, industrial slump

- 2019 LNG supply additions largest since the Qatari mega-trains

- US gas supply growth to exceed demand growth even with LNG exports

- Global solar growth slowing

- Shipping disruption looming - IMO 2020

- New Russian gas pipeline advantage over Ukraine

- US coal demand to decline again in 2019

- Growth in new refineries and complex capacity likely to weigh on refinery margins especially in Asia

Year 2019 will certainly be one of transition for crude and refined oil products as it will lead into 2020 when roughly three million barrels per day of high-sulfur fuel oil must be "destroyed" (including enhanced usage of HSFO in power generation) due to the International Marine Organization (IMO) mandate of eco-friendly shipping fuels in use at sea. A similar amount of middle distillate/low sulfur fuel must be "created" (by refinery changes and by running more crude oil. The increase in refinery capacity between now and 2020 is large, but mostly needed to cover normal demand growth. Expect prices of light sweet crudes to be bid up in 4Q19.

One of the key lessons learned in 2018 (painfully by some), is that market sentiment can shift violently without much change in fundamentals, requiring a steady, holistic perspective. See the Executive Summary of the S&P Global Platts Analytics special report 2018 Review and 2019 here.

Media Contacts:

Global, Americas, Asia: Kathleen Tanzy, + 1 917 331 4607, kathleen.tanzy@spglobal.com

About S&P Global Platts

At S&P Global Platts, we provide the insights; you make better informed trading and business decisions with confidence. We're the leading independent provider of information and benchmark prices for the commodities and energy markets. Customers in over 150 countries look to our expertise in news, pricing and analytics to deliver greater transparency and efficiency to markets. S&P Global Platts coverage includes oil and gas, power, petrochemicals, metals, agriculture and shipping.

S&P Global Platts is a division of S&P Global (NYSE: SPGI), which provides essential intelligence for individuals, companies and governments to make decisions with confidence. For more information, visit www.platts.com.

SOURCE S&P Global Platts