Press Releases

Will the last throttle body manufacturer please turn out the lights?

SOUTHFIELD, Mich., May 1, 2023 /PRNewswire/ -- The time for denial is over. There are still suppliers of parts related to internal-combustion engines that are steadfast in their belief that the looming (and eventual) shift away from ICE toward any number of battery-electric propulsion formats is just a passing fad.

In their view, scores of OEMs, suppliers, dealers, and infrastructure partners have it completely wrong. That the billions in investment earmarked in virtually every major global market to build a new ecosystem is capital that is misallocated. That years of industry strategic moves and government regulations to position both nations and organizations for success in a battery-electric vehicle future are in haste.

Or, conversely, these legacy players may recognize that change is coming, but their corporate strategy is paralyzed by the surge of electric vehicle introductions.

They will be the losers when the next history of the auto industry is written.

While the pace and timing of this transition will be variable (read: lumpy), working under the premise of, "When, not if," should be the rally cry among the supplier base. This existential threat is already separating winners from losers -- whether they know it or not.

That's not to say the shift will be immediate, or that there won't be strong revenue streams to be had during this transformation. It will be protracted, and there are still tremendous profits to be made in the internal combustion space over the next couple of decades -- especially in the aftermarket.

After all, there are 1.3 billion internal combustion cars on the world's roads today, according to S&P Global Mobility estimates, and they aren't going to just vanish. Nor will BEVs take dominant share of the vehicles in operation for many years to come. But the shift is happening.

There are thousands of moving parts in the internal-combustion powertrain; battery electric vehicles have only a couple dozen. As a result, there will be a brutal shakeout and consolidation among engine, transmission, and driveline suppliers in addition to those in the fuel and exhaust systems sectors. The victims will be those who failed to plan ahead and listen to their customers.

As S&P Global Mobility sees it, those suppliers have four strategic choices:

- Divest from ICE, and shift to BEV components

- Milk the cash cow dry, while shrinking to an eventual shutdown

- Double down to become the dominant part supplier

- Position to be acquired

We will delve into the strategic ramifications of those choices, but first, a bit of history to set the gameboard to enable the decision-making process to begin.

The ICE-to-BEV transition is but one recent concern

The last handful of years have been unkind to light-vehicle component suppliers. Impacted by numerous disruptions and resultant erratic production volumes, the recent past has been more of a daily dumpster fire for supplier executives.

These mounting issues date back to early 2019 when once surging production volumes in China started to take a breather. According to S&P Global Mobility's light vehicle production research, Mainland China's annual volumes more than doubled to 26.6 million units between 2009 and 2018. But in 2019, volume slipped greater than 8% in one year and started an endless cascade of industry hurdles. Meanwhile, in North America, a late-2019 labor spat between General Motors and the UAW impacted scores of suppliers.

Then COVID hit, shuttering output for almost two months and crippling output for months to come. North American production slipped more than 20% in 2020. In many respects, the light vehicle production ecosystem has been reeling ever since, with few opportunities to come up for air.

Macroeconomic impacts started with ongoing semiconductor shortages for automotive-grade chips, followed by growing geopolitical trade tensions spiked by Russia's invasion of Ukraine, and capped by mounting labor availability issues. Though abating in amplitude of late, the industry will still feel these extraneous pressures through the end of 2023.

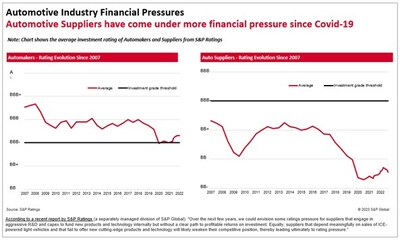

But there were industry-specific issues as well. Suppliers were sandwiched between OEMs and their capability to lever vehicle prices/content upwards with end customers. Meanwhile, upstream material suppliers gained new pricing leverage due to the strength of demand as COVID abated. As an example, hot rolled steel is expected to rise 14% from last fall to the end of next year. As a result, tier 1 and 2 suppliers are caught in the middle.

Add to this other external cost pressures such as wages, logistics, and energy prices - suppliers are longing for the days of predictable output and cost stability. Adding to the equation are rising interest rates, which increases the cost of debt service among lending institutions with a renewed focus on debt quality.

The supplier cost squeeze has limited strategic options

Why the history lesson, the circumstances of which would hurt the industry even if there weren't a fundamental shift in its propulsion method? Because it magnifies the situation.

Even if it were the best of the times, an industry experiencing this sort of transformation from ICE to BEV propulsion would have its fair share of participants throwing in the towel. Add the aforementioned financial pressures and risk dynamics impacting the industry since 2019, and you have a recipe for significant industry turnover.

This frantic pace of change and its inherent risks for capital in a rising interest rate environment, the skills/process transition required, and the advantages gained by innovators and first movers in this new environment is head spinning. Emerging from this unfortunate timing combination of significant competitive challenges will be an ecosystem which will not resemble the one in which we entered this century. Despite the challenges, nimble industry participants -- be they OEMs, suppliers or dealers -- will leverage this tumult to their advantage.

Early evidence of a looming propulsion transition emerged even before 2019. Both China and the European Union understood (albeit for differing reasons) that legislating vehicle emission reductions through the coming decade was going to upend the competitive dynamics of their home market vehicle manufacturers and the suppliers which served them.

As a result, OEMs will be required to devote a substantial share of capital expenditures to battery-electric propulsion systems and platform structures. They are understandably reducing their focus and resources on traditional ICE systems due to limited payback and slowly abating volumes/utilization.

Back in 2015, the number of new engine combinations (family/program) launched for production in North America reached 13; in 2025, this will plummet to two, according to S&P Global Mobility forecasting data. The result of this transformation is predictable. Impacted suppliers in these ICE-focused systems are being asked to extend programs past their expected life cycles, slow efforts to integrate innovation, and search for efficiencies to lower/control costs.

Some ICE powertrain suppliers may discover they are unable to pivot to a BEV world. One option for entrapped medium-sized suppliers may be to ride an ever-decreasing ICE revenue stream until the business is unsustainable; Wall Street tends to look unkindly on that business model. Another path is to become the dominant supplier in a niche segment - be it for throttle bodies, ignition coils, exhaust manifolds, or some such - and hope that the aftermarket business is sufficient to keep the business afloat.

While traditional propulsion systems suppliers face these challenges, an opportunity is emerging for others to build new value chains and differentiate innovations and competitive advantages as first movers.

The new world: Think global, source local, build local

Though the number of new BEV platforms (all-new structures and processes) has primarily been initiated in China and the European Union through this decade so far, North America is catching up quickly. Installation of new, highly flexible BEV platforms is already underway in North America. According to S&P Global Mobility, 84 BEV nameplates, built at 47 vehicle production lines, are forecast by 2025 - and North American numbers may surge due to benefits incurred under the Inflation Reduction Act (IRA). For many of these offerings, development and component sourcing occurred years ago.

The emerging BEV production ecosystem has few similarities to that of today's ICE-focused version. For decades the advantages of a globally-rationalized industry were touted as optimal - the tide is now turning.

For instance, the days of efficiently sourcing engines and transmission from over an ocean has given way to propulsion systems (battery cells and enclosures) produced regionally. We are entering a BEV chain based on localism - usually within a couple hundred miles of the final-assembly plant. While this new supply chain was forming well ahead of the recently enacted IRA, financial incentives will drive even greater value-add through the upstream battery inputs (anode & cathode material) within North America.

What's more, geopolitical risks, potential trade frictions (such as between the United States and China), sustainability and ESG concerns, and growing logistics issues will drive tomorrow's supply chain even closer to home factories. Suppliers will need to adapt to nearer supply networks, an even-greater concentration on efficiency, and labor stability to build robust upstream chains.

Irrational exuberance and overcompensation

There also is a danger in changing course too quickly. What happens to suppliers that go all-in on an electrification push that does not meet expectations?

After all, it's an industry truism that, if you added up each automaker's calendar year sales projections, the US market would be 22 million vehicles. Of course, it has never come close to that.

Mike Wall, executive director of automotive analysis, warns that sort of overexuberance in sales projections seen with internal-combustion vehicles could happen just as easily with electric vehicles. And suppliers could end up holding the bag.

"Automakers are making some big production projections. One will say, 'We're going to sell 1 million EVs.' Then the next one says, 'We're going to sell 2 million.' And suppliers are being told to plan for this much capacity," Wall said.

"If you are a supplier told to plan for a vehicle with 150,000-unit volume, what if it happens to come in at 50,000? Besides altering the basic profit potential for the part, if you amortize tooling and development costs into your piece costs, it will take much longer to recover those costs, if it ever happens. If you are a supplier, you won't be selling at 100% capacity at job one," Wall added.

These are important considerations as suppliers venture into the quoting process for any new business, particularly electrified vehicles.

Additionally, going it alone may not be the optimal path. Reacting to new opportunities through alliances and partnerships will be key as the speed of vehicle development rises. A new competitive dynamic will emerge as reliance on past advantages gives way to a new definition of success or failure.

Those suppliers slow to transition to BEV technologies have missed the initial surge. Remember that there are three timelines in the industry:

- Development (which occurs up to five years before start of production)

- Tooling for production (two to three years before start of production); and

- Service/aftermarket requirements once in service.

It's a harsh assessment, but given the time-factors involved, a supplier's strategic perspective needed to be in play years ago. In an industry built on relationships, the need to break into the BEV supplier base will be frenetic. But BEV propulsion uses a fraction of the parts required for internal combustion, and as a result, more than a few suppliers will be left standing without a chair when the music stops. The level of displacement and disruption will be significant. Planning ahead is critical to survival.

Please contact automotive@spglobal.com to find out more information around our insights to help you make data-driven decisions with conviction.

Editor's Note: This report is from S&P Global Mobility, and not S&P Global Ratings, which is a separately managed division of S&P Global.

About S&P Global Mobility (www.spglobal.com/mobility)

At S&P Global Mobility, we provide invaluable insights derived from unmatched automotive data, enabling our customers to anticipate change and make decisions with conviction. Our expertise helps them to optimize their businesses, reach the right consumers, and shape the future of mobility. We open the door to automotive innovation, revealing the buying patterns of today and helping customers plan for the emerging technologies of tomorrow.

S&P Global Mobility is a division of S&P Global (NYSE: SPGI). S&P Global is the world's foremost provider of credit ratings, benchmarks, analytics and workflow solutions in the global capital, commodity and automotive markets. With every one of our offerings, we help many of the world's leading organizations navigate the economic landscape so they can plan for tomorrow, today. For more information, visit www.spglobal.com/mobility.

For media information, contact:

- Michelle Culver, Executive Director, Public Relations, S&P Global Mobility

michelle.culver@spglobal.com

![]()

SOURCE S&P Global Mobility