Press Releases

NEW YORK, Nov. 15, 2023 /PRNewswire/ -- Near term headwinds will hinder the energy and metals sectors' Energy Transition efforts in 2024, according to a new S&P Global Market Intelligence report released today. The newly published 2024 Commodities outlook: Near-term risks abound for energy transition, critical minerals is part of S&P Global Market Intelligence's Big Picture 2024 Outlook Report series.

The new report, published in partnership with S&P Global Commodity Insights' research team, highlighted key trends facing the energy, utility, and metals sectors in 2024. According to the report, persistent high interest rates and macroeconomic uncertainty will negatively impact project decisions over the coming year, which dovetailed against complex regulatory pathways, will slow the effort to shift away from fossil fuels.

"2023 has been a year of challenging conditions for companies in the energy and metals sectors, marked by macroeconomic and geopolitical uncertainty. Amid continued high interest rates, near-term demand weakness and persistent regulatory challenges, 2024 will see continued cause for concern among many participants, even though ongoing efforts geared towards the global energy transition should yield benefits in the medium term," said Mark Ferguson, Director of Metals & Mining Research at S&P Global Commodity Insights.

Key highlights from the report include:

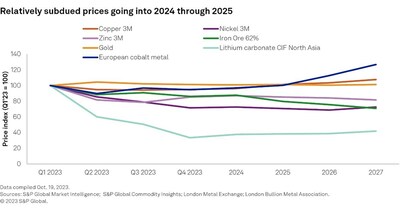

- High interest rates, persistently elevated inflation and slowing economic growth are key headwinds to energy transition projects heading into 2024, with these factors also suppressing demand for critical minerals and contributing to tempered metals prices into 2025.

- Shifting government policies and complex regulatory systems foreshadow changes to the business strategies of mining, utility, and energy companies. In the US, a multi-tiered and often conflicting regulatory environment could slow the momentum behind the domestic energy transition.

- Geopolitical tensions are also hindering progress as increasingly protectionist attitudes delay new developments and add costs to electric vehicles, among other key efforts in the transition.

To request a copy of the 2024 Commodities Outlook: Near-term risks abound for energy transition, critical minerals, please contact press.mi@spglobal.com.

S&P Global Market Intelligence's opinions, quotes, and credit-related and other analyses are statements of opinion as of the date they are expressed and not statements of fact or recommendation to purchase, hold, or sell any securities or to make any investment decisions, and do not address the suitability of any security.

Statements by persons who are not S&P Global Market Intelligence employees represent their own views and opinions and are not necessarily the views of S&P Global Market Intelligence.

About S&P Global Market Intelligence

At S&P Global Market Intelligence, we understand the importance of accurate, deep and insightful information. Our team of experts delivers unrivaled insights and leading data and technology solutions, partnering with customers to expand their perspective, operate with confidence, and make decisions with conviction.

S&P Global Market Intelligence is a division of S&P Global (NYSE: SPGI). S&P Global is the world's foremost provider of credit ratings, benchmarks, analytics and workflow solutions in the global capital, commodity and automotive markets. With every one of our offerings, we help many of the world's leading organizations navigate the economic landscape so they can plan for tomorrow, today. For more information, visit www.spglobal.com/marketintelligence.

Media Contact

Amanda Oey

S&P Global Market Intelligence

+1 212-438-1904

amanda.oey@spglobal.com

![]()

SOURCE S&P Global Market Intelligence